Atlas Energy Solutions (AESI)·Q4 2025 Earnings Summary

Atlas Energy Solutions Q4 2025 Earnings: Revenue Beat, But Stock Plunges 11% on Power Pivot Uncertainty

February 24, 2026 · by Fintool AI Agent

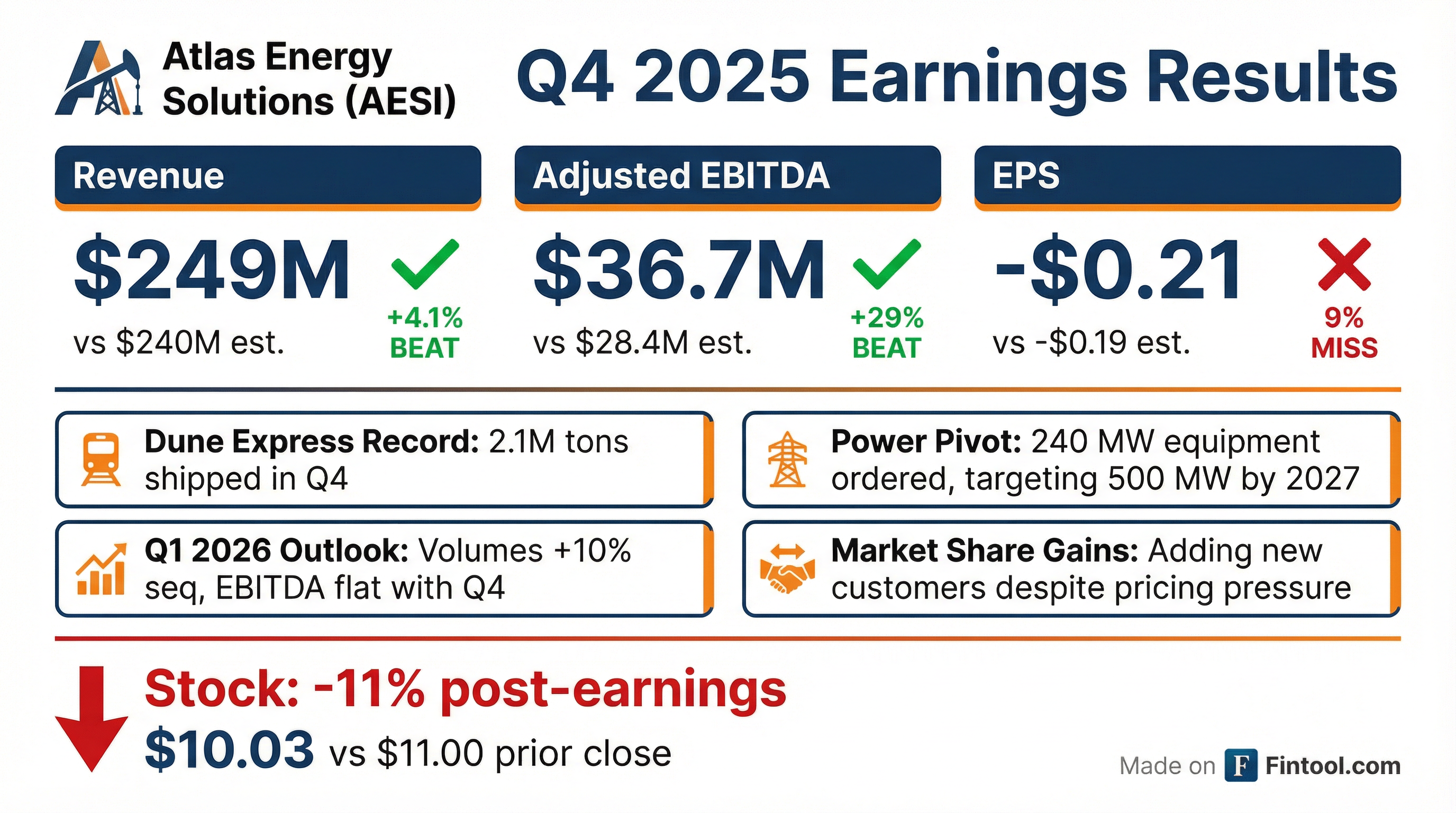

Atlas Energy Solutions delivered mixed Q4 2025 results, beating on revenue and EBITDA but posting a wider-than-expected loss as the Permian sand and logistics market remains in what management called "unsustainable" pricing conditions. The stock plunged 11% on the report as investors weighed the near-term pain against the company's ambitious pivot into behind-the-meter power generation.

The quarter marked the lowest point in what has been a difficult year for Atlas's core business, with EBITDA margins compressing to 15%—down from 20% for the full year and a far cry from the 36% margins posted in Q1 2024.

Did Atlas Energy Solutions Beat Earnings?

Revenue: Beat. Atlas posted $249.4 million in revenue versus consensus of $239.5 million, a 4.1% beat driven by stable volumes and continued adoption of the Dune Express conveyor system.

Adjusted EBITDA: Beat. The company delivered $36.7 million in Adjusted EBITDA versus consensus of $28.4 million—a 29% beat that exceeded management's own initial expectations.

EPS: Miss. Normalized EPS came in at -$0.21 versus consensus of -$0.19, a 9% miss reflecting the challenging margin environment and elevated interest expense.*

*Values retrieved from S&P Global

How Did the Stock React?

AESI shares dropped 11% on the day of the earnings release, falling from $11.00 to $10.03. The stock is now trading below its 50-day moving average of $10.79 and 200-day average of $11.59.*

The selloff reflects investor concerns about:

- Continued margin compression — EBITDA margin of 15% vs. 20%+ historically

- Pricing headwinds — Sand ASP expected to drop to $18/ton in Q1 from $19.85

- Power business execution risk — Large capital commitments with contracts not yet signed

*Values retrieved from S&P Global

What Did Management Guide?

Q1 2026 Outlook:

CFO Blake McCarthy noted that while volumes are growing, pricing headwinds and the January winter storm will pressure Q1 margins. The company expects to exit Q1 "at a higher run rate in March versus January."

Full Year 2026: Management was intentionally vague on second-half guidance, noting that customers are "taking a wait-and-see approach" with completion schedules given oil price uncertainty. Many customer budgets are built around $50-$55 WTI.

What Changed From Last Quarter?

The Power Pivot Accelerates

The most significant development is Atlas's aggressive move into behind-the-meter power generation—a strategic transformation from pure-play sand provider to diversified energy infrastructure company.

Key announcements:

- 240 MW ordered — Power generation equipment arriving late 2026

- 500+ MW target by 2027 — Targeting deployment across E&P, data centers, and manufacturing

- $375M lease facility — Non-dilutive financing secured with Eldridge

- High-teens unlevered IRR — Target returns on behind-the-meter projects

- 5-15 year contracts — Long-term cash flow visibility versus volatile oilfield services

CEO John Turner emphasized the urgency of the opportunity: "Rising residential electricity prices, up 7.4% in 2025 alone, are creating political and economic pressure for more affordable, dependable alternatives. This dynamic is pushing developers to secure dedicated behind-the-meter power assets."

Sand Pricing Hits "Unsustainable" Levels

Management was blunt about the state of the Permian sand market:

"Logistics pricing in the Permian has fallen to completely unsustainable levels, well below those seen during COVID. To compete with the Dune Express, we have seen increasingly irrational behavior from some of our logistics competitors, which we believe sets both them and their customers up for eventual problems and disruptions."

— Blake McCarthy, CFO

Despite the challenging environment, Atlas gained market share by leveraging its cost advantages from the Dune Express conveyor system and low-cost mines. The company expects volumes to grow year-over-year in 2026.

Dune Express Hits Records

The company's flagship conveyor system continued to perform:

- Record Q4 shipments: 2.1 million tons

- November record: 760,000 tons (single month)

- 21+ million truck miles eliminated since January 2025 launch

- 2026 target: 10+ million tons via Dune Express

Key Financial Trends

*Values retrieved from S&P Global

The table reveals the dramatic margin compression over the past year, with EBITDA margins falling from 36% in Q1 2024 to just 11-15% in recent quarters.

Q&A Highlights

On Power Business Timing

Analyst: "What's taken a little while on getting [power equipment] contracted?"

John Turner: "These just aren't generator rental agreements. These are actually... You have to go in and do planning, engineering. You have to do, you have to line up all the equipment. There's a lot of different things that you have to do on that front."

On Grid Interconnection Delays

Tim Ondrak (President of Power): "What we're hearing from utilities... is anywhere from 2028 to 2034 for a load to interconnect. When a customer looks at what their power need is... they need to look at what they call a bridge solution."

On Sand Market Recovery

Blake McCarthy: "It's only gonna take a very small increase in completions activity for pricing to move. The supply demand for sand in the Permian is much tighter than the market realizes, especially for dry sand."

Capital Allocation & Balance Sheet

*Values retrieved from S&P Global

The company achieved its $20 million annualized cost savings target through headcount optimization, equipment rental reductions, and procurement savings.

New dredges ("Twinkle dredges") are scheduled for commissioning in Q2 2026, which should improve plant operating costs by approximately $1/ton across the complex.

Forward Catalysts

Key Risks to Monitor

- Power execution risk — Large capital commitments with contracts not yet announced

- Oil price sensitivity — Customer budgets assume $50-55 WTI; second-half visibility limited

- Pricing pressure — Sand/logistics pricing at multi-year lows with "irrational" competition

- Interest expense growth — Net interest rising from $16.5M to $22M per quarter through 2026

- Weather disruption — January storm cost ~$6M in lost EBITDA

The Bottom Line

Atlas Energy Solutions is in transition. The core sand and logistics business is navigating through a painful pricing trough, while management aggressively pivots toward the higher-margin, longer-duration opportunity in behind-the-meter power generation.

The bull case: Sand pricing is at unsustainable levels and must recover; the Dune Express provides structural cost advantages; and the power business could transform the company's earnings quality with 5-15 year contracted cash flows.

The bear case: Power contracts remain unsigned, execution risk is high, and the core business continues to deteriorate. The stock's 11% drop suggests investors want to see contracts before giving management credit for the pivot.

Executive Chairman Bud Brigham summed up the thesis: "The Atlas investment story is more exciting than ever. Chronic underinvestment in exploration spending, coupled with shale's maturation and steep decline rates, sets the stage for what I believe will be a prolonged upcycle."

This analysis was generated by Fintool AI Agent based on Atlas Energy Solutions' Q4 2025 earnings call held on February 24, 2026. For the full transcript, visit AESI Transcripts.